Market Report

Learn more about all important trends in the precious metals markets in our market reports on a regular basis.

Latest Issue of the Market Report

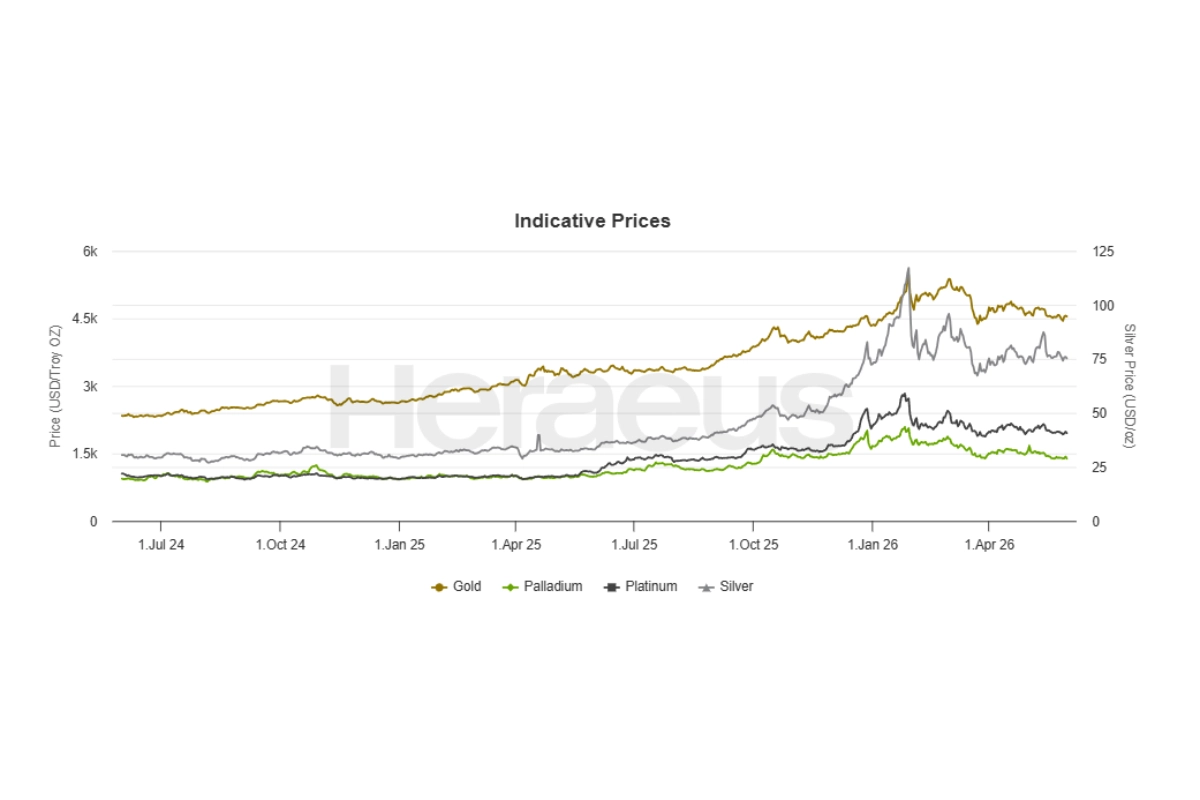

No. 29 | 10th August 2026: Precious Metals Surge as Easing Energy and Rate Pressures Boost Market Sentiment

Gold, silver, platinum, and palladium posted strong gains last week amid falling oil prices, softer interest rate expectations, and continued central bank gold purchases. Improved industrial demand prospects and supportive supply dynamics further strengthened sentiment across the precious metals complex.

Register for our Market Report

You would like to receive our market report by e-mail? Then register now using the form provided below.

After submitting the form, you will receive an activation link via e-mail. Please confirm your registration by clicking on the link. You can, of course, withdraw this consent at any time. At the end of each newsletter you will find a corresponding unsubscribe link.